You financed a 2024 Nissan Rogue last fall. Your lender required full coverage, which you got, and the monthly premium fit your budget. Then your renewal notice arrived this spring with a 4% increase your carrier attributed to “rising repair costs.” It’s not an accident that the timing coincides with broad tariff increases on imported vehicles and auto components that took effect in 2025. The connection between trade policy and your insurance requirement isn’t obvious, but it’s direct, and it has specific implications for anyone financing a vehicle in 2026.

This article covers the mechanism — how tariff-related repair cost increases flow through to the lender insurance requirements on your financed car, what lenders actually mandate versus what dealers sell you, and how to keep your coverage budget in check without accidentally falling short of what your loan agreement requires.

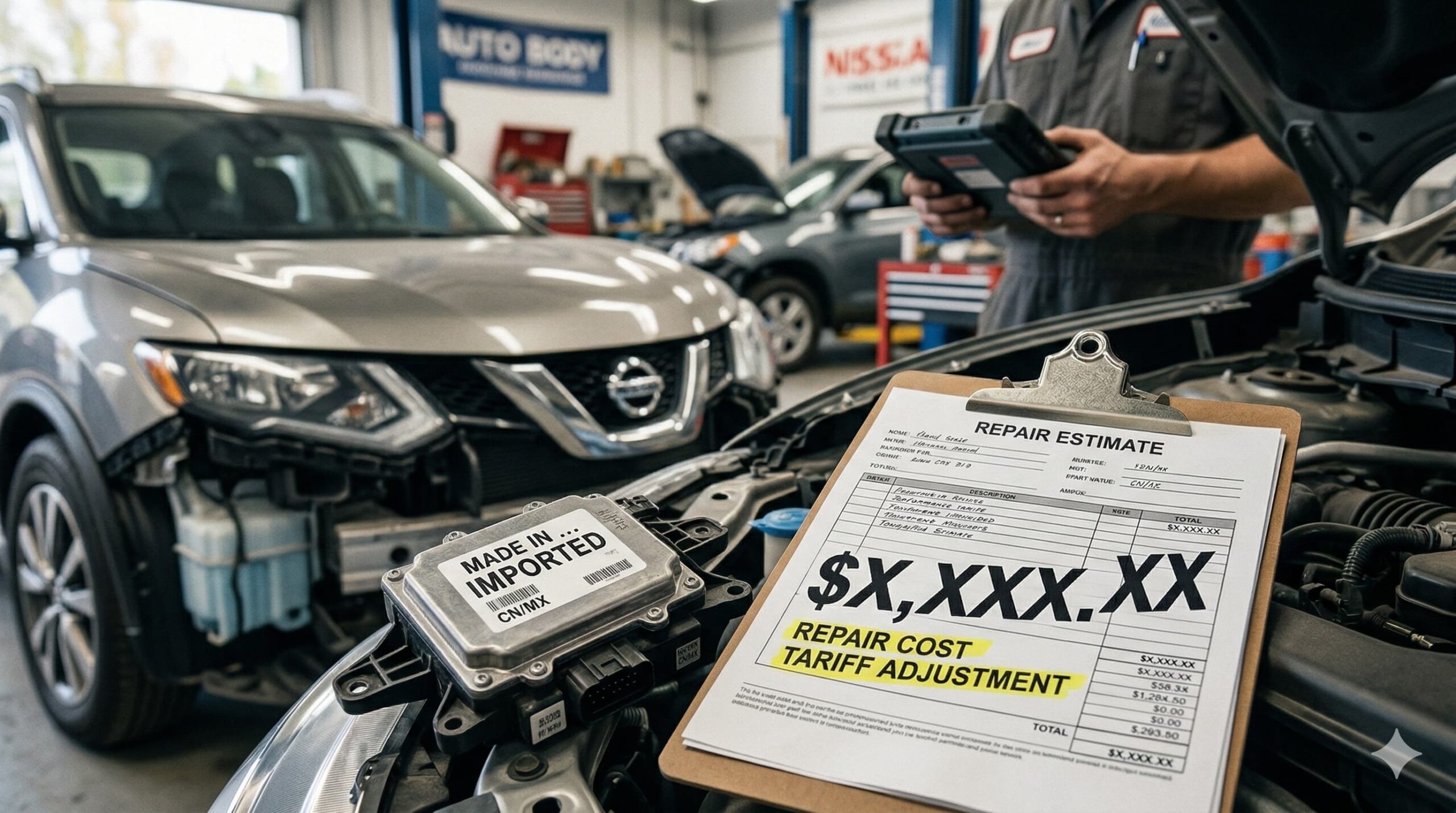

How Tariffs Are Raising Auto Repair Costs in 2026

The 2025 tariffs on imported vehicles and auto components created a cost increase that ripples through the repair chain. Parts manufactured overseas, which includes components for most vehicle makes sold in the US, cost more to import. Body shops, mechanical repair facilities, and insurers all absorb those increases. When a carrier pays a claim, the higher parts costs come directly off their loss ratio, which drives premium adjustments at renewal.

Insurance industry analysts are projecting 1-4% state-wide premium increases in 2026 specifically tied to tariff pass-through costs, with the full impact expected to continue accumulating through 2026 and beyond. That range sounds small until you apply it to the full coverage premiums that lenders require on financed vehicles, which already averaged $2,144 nationally heading into 2026, per ValuePenguin data. A 3% increase on a $2,144 annual premium is about $64 per year, or roughly $5 per month. Modest individually, but it compounds alongside the loan payment, property taxes, and fuel costs that make up the full cost of vehicle ownership.

Key takeaway: Tariff-related repair cost increases don’t hit your premium directly — they raise the cost of claims, which carriers then pass through at renewal. The connection is real even when it’s not labeled that way on your renewal notice.

Why financed vehicles are the ones to watch

On an unfinanced vehicle you own outright, the coverage decision is yours. You can legally carry state minimums, accept the risk of a large out-of-pocket repair, and drop comprehensive and collision if the vehicle value doesn’t justify the premium. Lenders remove that flexibility. Your loan agreement specifies minimum coverage levels, typically comprehensive and collision with deductibles at or below a set threshold, for the duration of the loan. When repair costs rise and carriers respond by increasing full coverage premiums, that cost is largely non-negotiable for financed vehicle owners.

What Lender Insurance Requirements Actually Specify

Lender insurance requirements are written into your loan contract and enforced through the lienholder status on your policy. The lender is listed as loss payee, which means claim payments for physical damage go to them first, to protect their collateral. Most lenders require:

- Comprehensive and collision coverage (not just liability)

- Deductibles typically at or below $500 to $1,000 depending on lender and vehicle value

- Coverage limits sufficient to cover the vehicle’s actual cash value

- The lender listed as lienholder/loss payee on the policy

What they do not universally require is GAP insurance, though many dealers present it as mandatory. GAP coverage protects you from owing more than the vehicle is worth after a total loss, which is a genuine risk on a loan with a low down payment. But it’s a product you choose — or decline — based on your loan-to-value situation. Dealer-sold GAP is frequently priced at $600 to $900 added to the loan; standalone GAP from your insurer typically runs $20 to $40 per year. The markup is significant. See our overview of loan insurance add-ons for the full breakdown of what’s required versus what’s being sold.

What happens if your coverage lapses

If your coverage drops below the lender’s minimum, or lapses entirely, lenders have the right to place “force-placed insurance” on your vehicle. This coverage is designed to protect the lender’s collateral, not you. It typically carries a much higher premium than market-rate full coverage, provides no liability protection for you, and is charged to your loan account. Force-placed insurance can add hundreds of dollars per month to your cost of ownership and goes into effect without much warning beyond a notice letter. The best protection against it is a policy that automatically renews and has the lender listed correctly as lienholder from day one.

How to Keep Your Required Coverage Budget Under Control

You cannot opt out of full coverage while carrying a loan, but you have meaningful control over what you pay for it. The lever most financed vehicle owners underuse is the deductible choice. Raising your comprehensive and collision deductible from $250 to $500 typically reduces annual premium by 8–12%. Moving from $500 to $1,000 can trim another 5–8%. The trade-off is a larger out-of-pocket if you file a claim, so the math only works if you have a cash reserve to cover that higher deductible in a worst-case scenario.

Key takeaway: On a financed vehicle, you can’t cut coverage — but you can cut the premium. Deductible adjustments and bundling your auto policy with renters or home coverage are the two levers with the most impact for financed vehicle owners.

Bundling auto with renters or home coverage

Bundling your auto policy with a renters or homeowners policy from the same carrier typically generates 8–15% multi-policy discounts. For a financed vehicle owner already paying mandatory full coverage, this discount applies to the exact coverage you’re required to carry. It’s one of the few ways to reduce the required cost rather than trading it for a different risk. The discount compounds across both policies, so the total savings often exceed what you’d get from shopping auto alone.

Telematics programs and financed vehicles

Usage-based insurance programs, where your carrier monitors driving behavior through a phone app or OBD device, have expanded significantly in 2026. Safe drivers can see discounts of 10–25% on their premium. For financed vehicle owners who can’t reduce coverage, a telematics discount is a direct way to lower the cost of the coverage you’re already required to carry. The practical caveat: telematics programs monitor hard braking, late-night driving, and rapid acceleration. If your commute includes a lot of highway driving or your schedule includes late-night returns, review what the program monitors before enrolling.

When to Reassess Your Coverage as the Loan Matures

Lender insurance requirements stay constant throughout the loan term, but the relationship between your vehicle’s actual cash value and the cost of insuring it changes as the vehicle depreciates. In the early years of a loan, the required comprehensive and collision coverage is protecting substantial collateral. In the final year of a 60-month loan, that same required coverage is protecting a vehicle worth significantly less.

Once your loan is paid off, the coverage decision returns to you entirely. If your vehicle’s actual cash value is below $8,000 to $10,000, the annual comprehensive and collision premium may exceed what you’d recover from a total loss claim. That’s the threshold at which many financial planners recommend dropping to liability-only. But while the loan exists, that calculation is irrelevant — the lender’s requirement governs. Our guide to how refinance timing can save you money explains how your loan term itself affects the total cost picture, including the insurance drag that comes with a longer loan.

Ready to compare your options? Get a free auto insurance quote and make sure your coverage meets your lender’s requirements.

Frequently Asked Questions

Can my lender force me to buy insurance from a specific carrier?

No. Lenders can require coverage minimums and deductible limits, and must be listed as lienholder, but they cannot require you to purchase from a specific insurer. You’re free to shop for the best rate meeting their requirements. If a dealer or lender implies otherwise, that’s a misrepresentation.

What happens to my lender’s coverage requirement if my car is totaled?

If your vehicle is totaled, the insurance payout goes to the lienholder first to satisfy your loan balance. If the payout is less than your remaining loan balance, you owe the difference. This is the scenario GAP insurance covers. Whether GAP is worth adding depends on how much you financed relative to the vehicle’s value at purchase.

Do tariff-related premium increases affect all vehicles equally?

No. Vehicles with higher proportions of imported parts, and vehicles where replacement parts are less commonly available domestically, tend to see larger repair cost increases. This disproportionately affects many popular Japanese, Korean, and European models. Vehicles with established domestic parts supply chains see less impact.

Can I negotiate the required deductible level with my lender?

Generally no. Lender deductible requirements are set by their underwriting guidelines and are written into the loan agreement at signing. You can always carry a lower deductible than required, but you cannot exceed the required maximum. If a lender requires deductibles at or below $500, carrying a $1,000 deductible would violate the loan terms.

How do I know if my policy lists my lender correctly as lienholder?

Your insurance declarations page lists all lienholders and loss payees. Request a copy of your declarations page after any policy change or renewal. Verify the lender’s name and address match exactly what’s on your loan agreement. Mismatches are more common than buyers expect and can create complications in a claim.