Auto loans often start with a clear monthly payment and a fixed term. But what happens near the end of that term can catch borrowers off guard. Balloon payments, residual balances, or unexpected fees can disrupt your budget if you are not prepared. Payment forecasting helps you avoid these surprises by showing how your loan behaves over time.

This guide explains how payment forecasting works, why it matters, and how it connects to smart budgeting and better loan decisions.

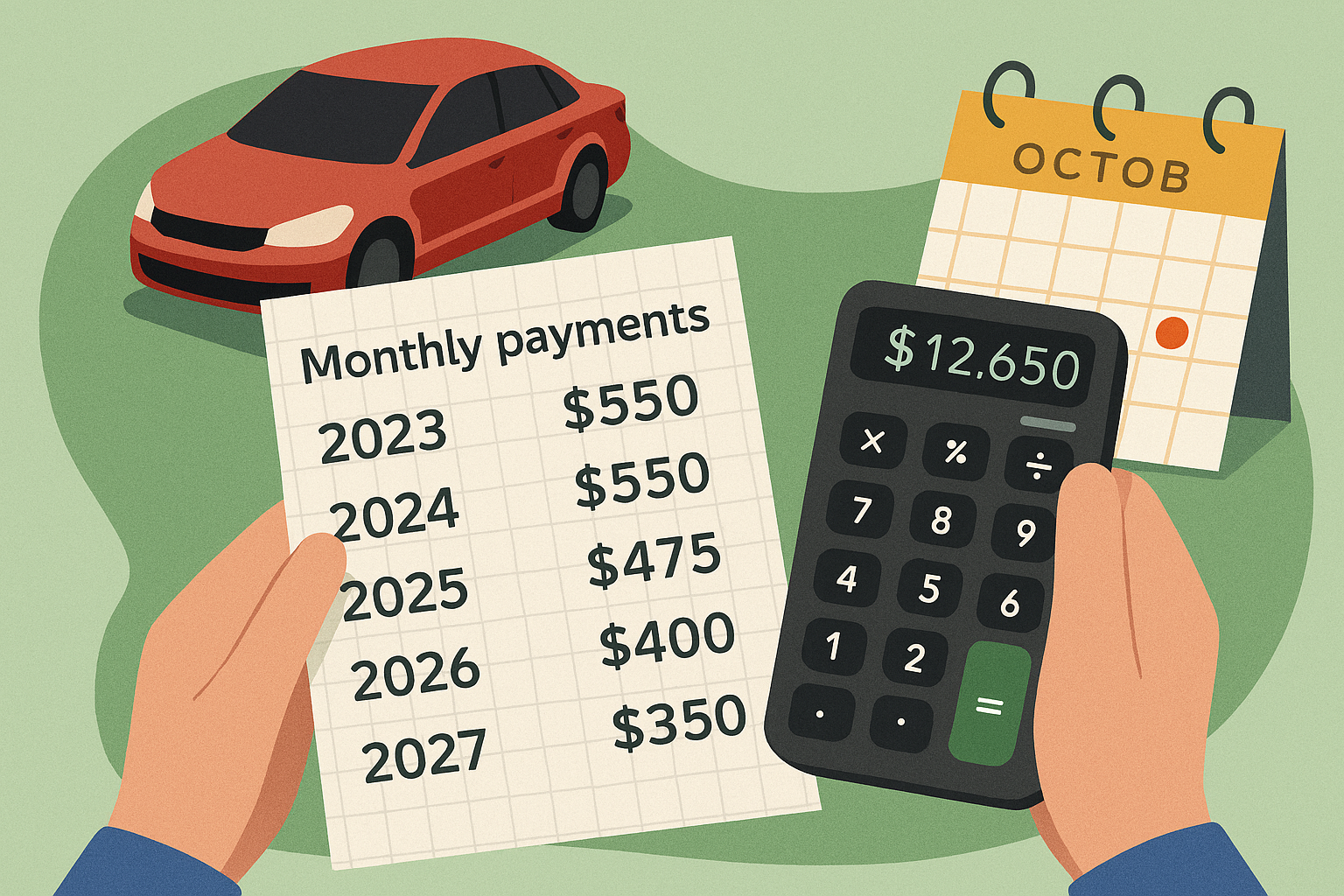

What Is Payment Forecasting?

Payment forecasting is the process of mapping out your loan payments from start to finish. It includes monthly amounts, interest costs, remaining balance, and payoff dates. The goal is to see how your loan evolves, not just what you owe today.

Forecasting tools use your loan details to generate a timeline. This includes:

- Monthly payment breakdowns

- Interest versus principal allocation

- Remaining balance at each point

- Total cost over the life of the loan

By seeing the full picture, you can plan ahead and avoid last-minute stress.

Why End-of-Term Surprises Happen

Many borrowers assume that making monthly payments means everything is covered. But some loans include terms that shift near the end. These may include:

- Balloon payments: A large lump sum due at the end of the loan.

- Residual value: Common in leases, where the car’s value affects your final payment.

- Deferred interest: Interest that builds up and becomes due later.

- Early payoff penalties: Fees for paying off the loan before the scheduled term.

Without forecasting, these details may go unnoticed. You may think you are close to being done, only to find a large balance still due.

How Forecasting Helps You Stay Ahead

Payment forecasting gives you control. It shows what to expect and when. This helps you:

- Plan for large payments in advance

- Avoid missed payments or late fees

- Decide when to refinance or adjust terms

- Track how extra payments affect your balance

For example, if you see a balloon payment coming in 18 months, you can start saving now or explore other options. If you notice that most of your payment goes to interest early on, you may choose to pay extra toward principal.

Connect Forecasting to Budgeting

Your loan does not exist in a vacuum. It affects your monthly budget, savings goals, and financial flexibility. Forecasting helps you align your loan with your broader financial plan.

Use forecasting to:

- Set monthly spending limits

- Build emergency savings

- Time large purchases around loan milestones

- Prepare for payoff or trade-in decisions

This keeps your finances balanced and reduces the chance of last-minute panic.

Use Digital Tools to Forecast Payments

Many lenders and financial apps offer payment forecasting tools. These platforms let you enter your loan details and see a full payment schedule. Some update in real time as you make payments or change terms.

Look for tools that:

- Show monthly breakdowns clearly

- Include interest and principal splits

- Let you adjust payment amounts

- Highlight payoff dates and total cost

These features help you stay informed and make smarter decisions.

Watch for Refinance Opportunities

Forecasting also helps you spot good moments to refinance. If your interest rate is high or your credit has improved, refinancing may lower your payments or shorten your term.

Use forecasting to track:

- When your balance drops below key thresholds

- How much interest you will pay over the next year

- Whether your current loan still fits your budget

This helps you improve your refinance timing and avoid locking into a new loan too early or too late.

Avoid Common Mistakes

Without forecasting, borrowers may:

- Miss balloon payments

- Overpay on interest

- Delay refinancing until rates rise

- Assume their loan ends when payments stop

These mistakes cost money and create stress. Forecasting helps you avoid them by showing the full path ahead.

Payment forecasting is not just a budgeting tool. It is a way to stay ahead of your loan and avoid end-of-term surprises. By tracking your payments, understanding your balance, and planning for key milestones, you protect your finances and make smarter decisions. Use forecasting tools early and often to stay in control and avoid costly missteps.