Most car buyers think about loan fit in terms of monthly payments and interest rates. But there is a deeper layer that often goes unnoticed. The rate at which a vehicle loses value over time directly affects how well your loan structure holds up. If you ignore depreciation behavior, you risk locking into a financial mismatch that erodes equity and limits flexibility.

Why Depreciation Should Shape Your Loan Strategy

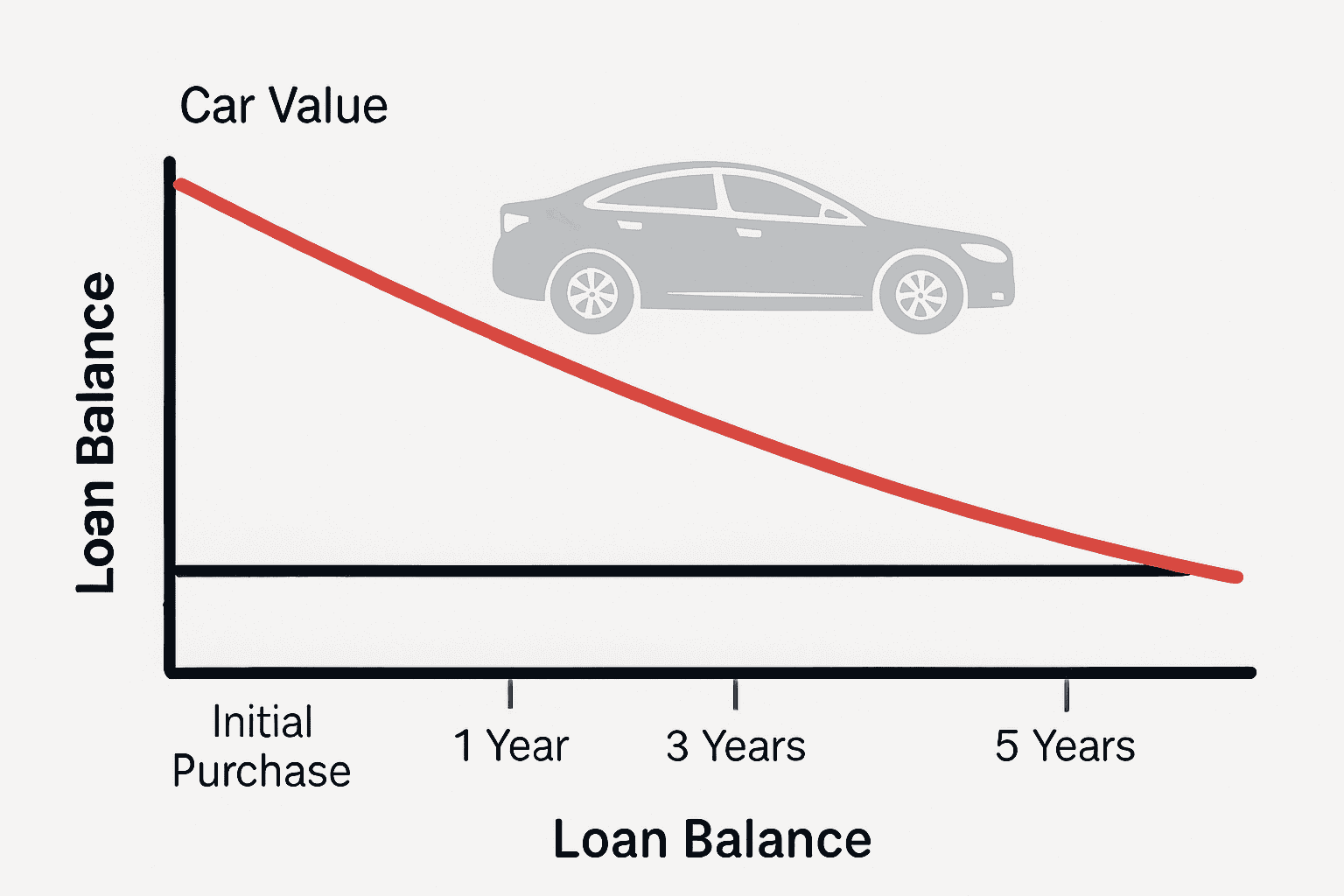

Depreciation begins the moment a vehicle is registered. The first year typically sees the steepest drop, followed by a slower decline in subsequent years. This pattern is not just a resale concern. It influences your loan-to-value ratio, your refinancing options, and your ability to exit the loan early.

A well-structured loan should account for how fast the vehicle loses value. If your loan term extends beyond the point where the car retains meaningful equity, you are paying into a structure that no longer reflects market reality. That disconnect can lead to negative equity, higher insurance costs, and limited trade-in leverage.

Model Year Timing and Loan Fit

One of the most overlooked timing factors is the model year transition. When a new model hits the market, the previous year’s inventory drops in value, even if it is still brand new. Dealers often offer discounts to clear out older stock, but those discounts do not always offset the accelerated depreciation.

If you finance a vehicle at the tail end of its model cycle, you need to adjust your loan terms accordingly. A shorter loan duration or a higher down payment can help you stay ahead of the depreciation curve. This ensures that your equity position remains stable even as the vehicle’s market value shifts.

Inventory Pressure and Loan Structuring

Dealers do not want vehicles sitting on the lot. A car that has been unsold for 60 days or more becomes a financial liability. That pressure often leads to price reductions and bundled incentives. While these deals can be attractive, they also signal that the vehicle may be approaching a steep value drop.

If you take advantage of a heavily discounted unit, make sure your loan reflects the adjusted price rather than the original MSRP. Structuring your loan around the real market value helps prevent overfinancing and protects your equity position over time.

Usage Profile and Depreciation Behavior

Depreciation is not just about age. It is also shaped by how the vehicle is used. A commuter car with low mileage will depreciate differently than a high-mileage SUV used for long trips. Service history, accident records, and even climate conditions can influence the rate of value loss.

Before finalizing your loan, forecast your usage profile. If you expect to drive more than average, consider a loan with early payoff options or a shorter term. This helps align your financing with the vehicle’s actual wear and tear, reducing the risk of being underwater on your loan.

Loan Fit Is Dynamic, Not Fixed

Loan fit is not a one-time calculation. It evolves as the vehicle ages and market conditions change. A five-year loan might look reasonable at the time of purchase, but if the car loses 40 percent of its value in the first two years, your equity position becomes fragile.

Use depreciation forecasts to model different loan scenarios. Compare short-term loans with higher payments against longer terms with lower monthly costs. Then layer in your ownership goals. If you plan to sell or trade in within three years, a seven-year loan is a poor match. You will owe more than the car is worth when it is time to exit.

Resale Planning and Depreciation Timing

Resale value is not just about demand. It is about timing. Selling during a steep drop means losing equity. Selling during a plateau allows you to retain more value. Understanding when your vehicle will hit those phases helps you plan your exit strategy.

This is especially important for buyers who lease with the intent to buy out or who finance with early payoff goals. If you misjudge the timing, you may find that your depreciation curve outpaces your equity growth, making it harder to refinance or switch vehicles.

Vehicle depreciation is not a background detail. It is a central factor in loan fit, equity management, and ownership flexibility. By understanding how value loss behaves over time, you can structure your loan to match reality—not assumptions.